Alexandre de Martino

Definition: Agtech, short for agricultural technology, refers to the use of technology to improve agricultural practices for better efficiency, productivity, and sustainability.

Feeding a growing population, without damaging even more land and climate are the main stakes to overcome in order to meet up with sustainable development goals. Through appropriate public policies, strategic financing, and innovative business models, agtech has the potential to propel a new green revolution.

Feeding the future

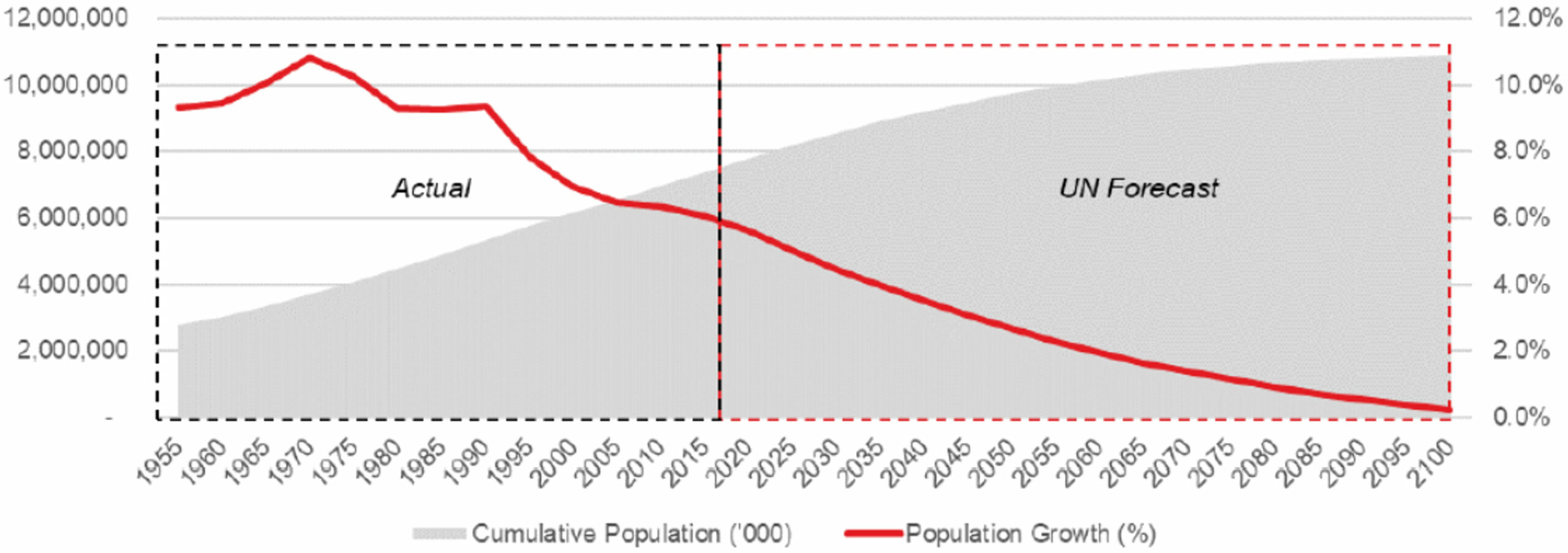

As the global population surges from 8 billion today towards an estimated 11 billion by 2100, the challenge of feeding everyone intensifies. Despite declining birth rates, advances in healthcare are prolonging life expectancies, particularly in developing regions, pushing the population numbers higher. By 2050, it is projected that we will need to increase food production by 50% to meet the demands of an anticipated 10 billion people. The Food and Agriculture Organization (FAO) further estimates that to maintain basic nutritional standards, food output must rise by 70%.

Exhibit 1: Global Population Forecast (‘000) and Growth (%)

Source: United Nations from NBT Technology Research

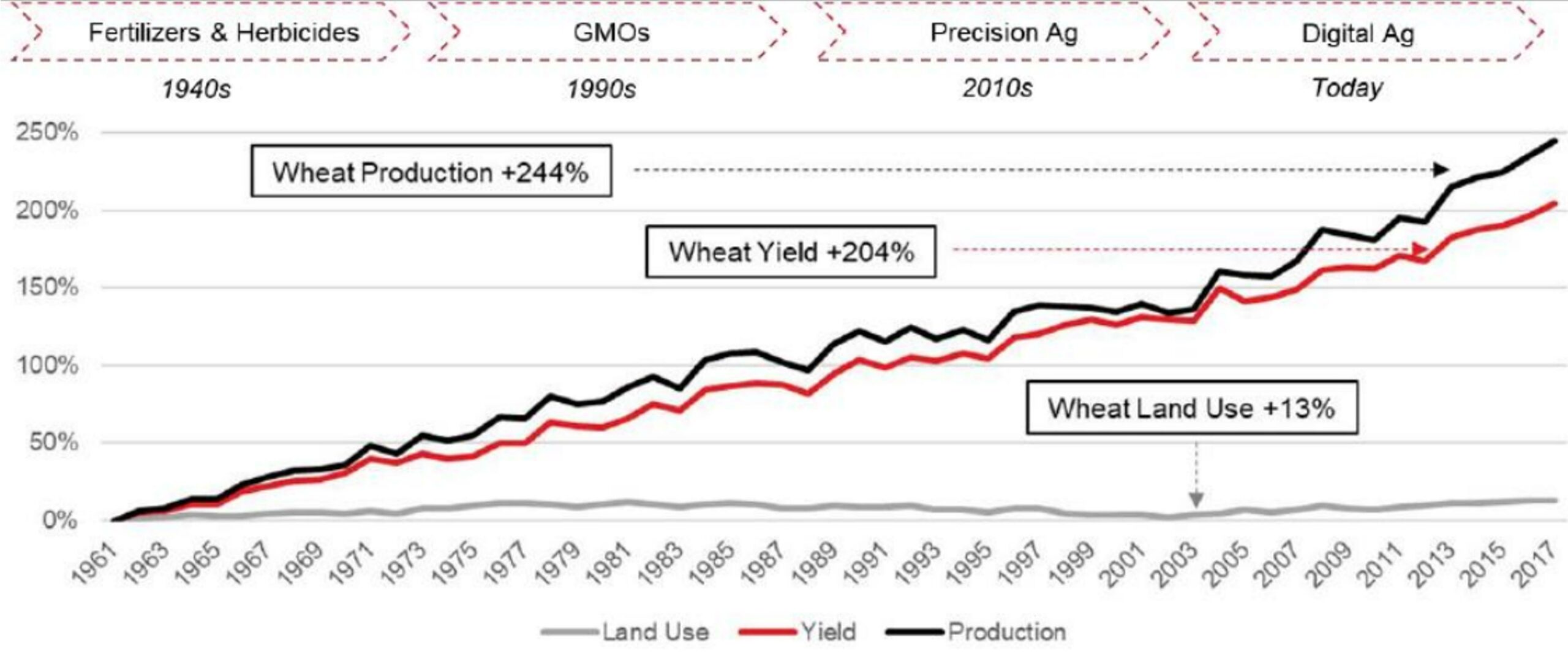

Overcoming decades of unsustainable agricultural practices

Over the past 50 years, the amount of land used for agriculture has not significantly increased. Despite this, agricultural production and crop yields, such as wheat, have seen remarkable improvements.

Exhibit 2: Agriculture has historically embraced innovation

Source: World Bank – World Development Indicators, OurWorldIn from NBT Technology Research

However, these advances come at a cost. The amount of global arable land is now declining due to erosion, deforestation, and pollution-factors largely driven by current agricultural practices. The extensive use of fertilizers and constant plowing have led to significant soil degradation.

Reducing the Food industry's greenhouse gas emissions in a

climate change era

The environmental impact of agriculture extends beyond soil degradation. In the broader context of climate change, the food industry is responsible for about one-third of global greenhouse gas emissions. This substantial contribution underscores the industry’s role in global warming and the importance of sustainable practices.

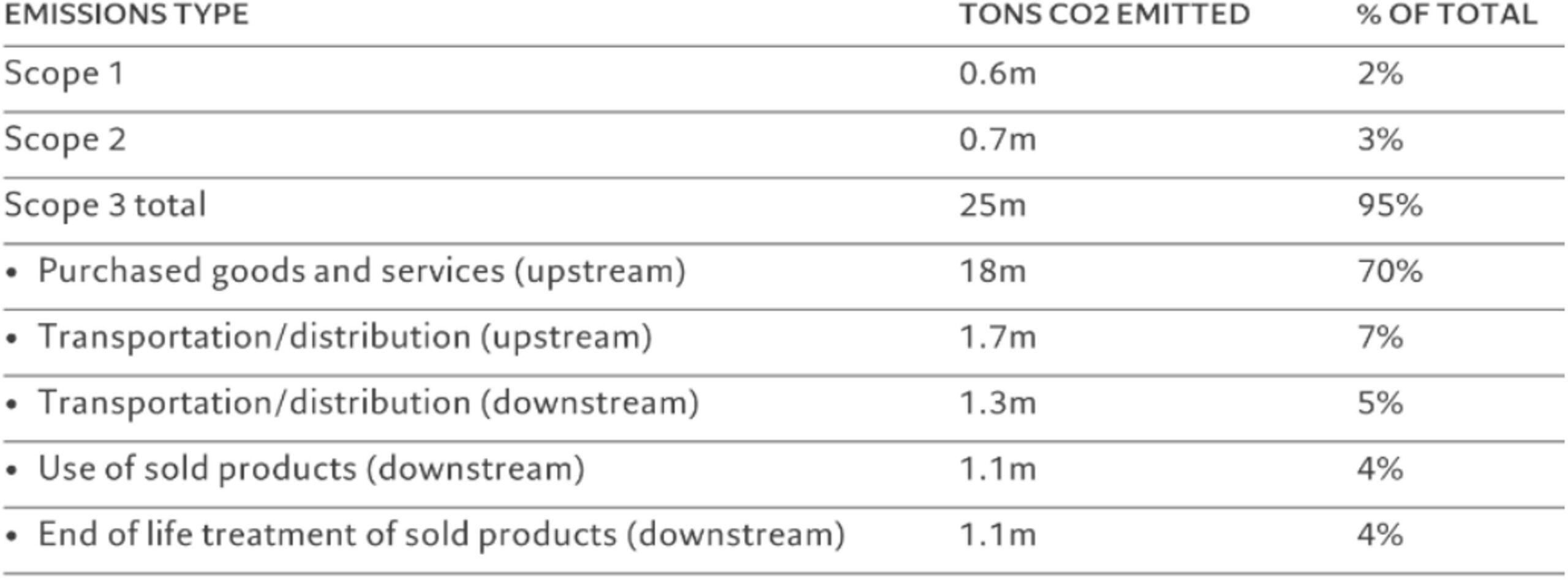

Furthermore, major food corporations such as Nestlé, Unilever, or PepsiCo work with hundreds of thousands of farmers, yet they often lack transparency into on-farm activities during the agricultural season. This is concerning because it is estimated that 85% of food-related greenhouse gas emissions originate at the farm level, categorized under scope 3 emissions in environmental reporting. This lack of visibility hampers efforts to monitor and reduce emissions, pointing to a need for more stringent oversight and sustainable collaboration between these corporations and their agricultural partners.

Exhibit 3: Kraft Heinz greenhouse gas emissions, by scope

Source: Kraft Heinz ESG report, 2021, annual data; figures given are CO2 equivalent

Why we believe now is the right time to invest in Agtech?

The farming industry is entering another cycle of innovation

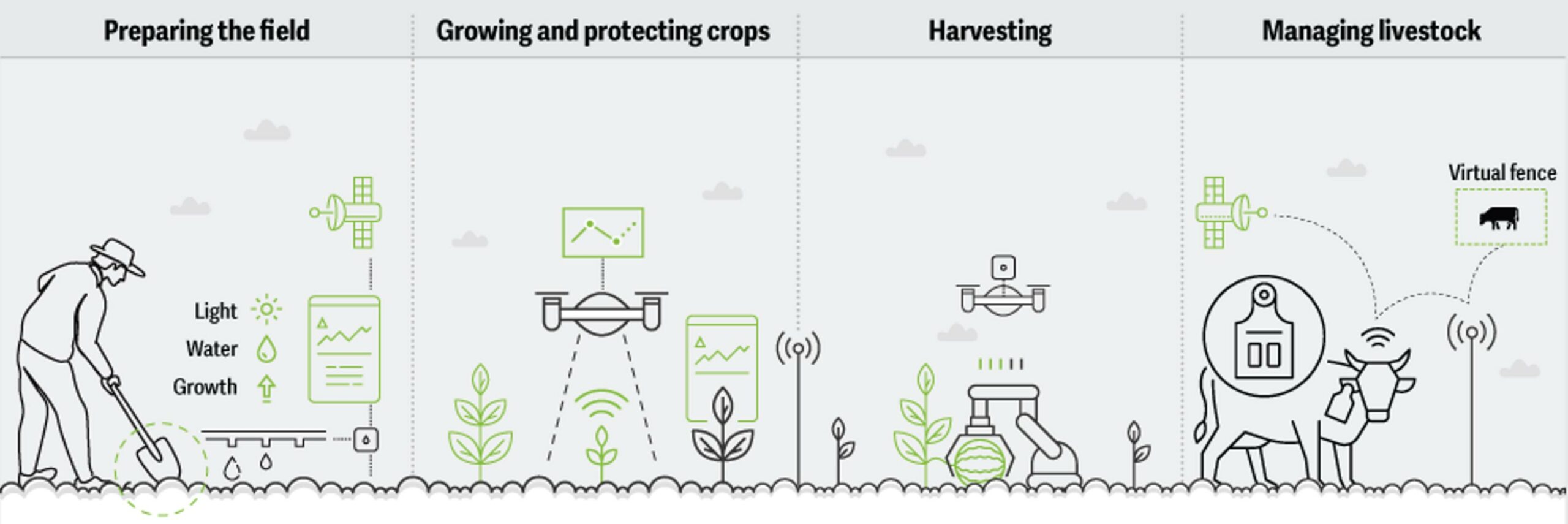

Over the past decade, advancements in rural connectivity and computing power have transformed precision agriculture into “digital agriculture” (digital ag). This new phase integrates IoT devices like smart weather stations and sensors, along with AI for predictive analytics, providing farmers with real-time data on various devices. These technologies help optimize daily operations, improve crop health, and aid in managing resources.

Exhibit 4: Innovative technologies across the farming lifecycle

Source: Deloitte

Leveraging regulatory momentum and corporate pledges from FMCG companies

Farmers worldwide are beginning to face more requirements to document and prove their sustainable practices to receive subsidies and meet their customers’ sustainability goals. With agriculture being the industry that receives the most subsidies—$540 billion according to the UN— there’s a growing emphasis on digital farming to support these efforts. Tightening regulations, like Europe’s aim for a 55% reduction in CO2 by 2030 and carbon neutrality by 2050, along with California’s carbon disclosure laws impacting over 16,000 companies, signal that this trend toward sustainable agriculture is likely to continue.

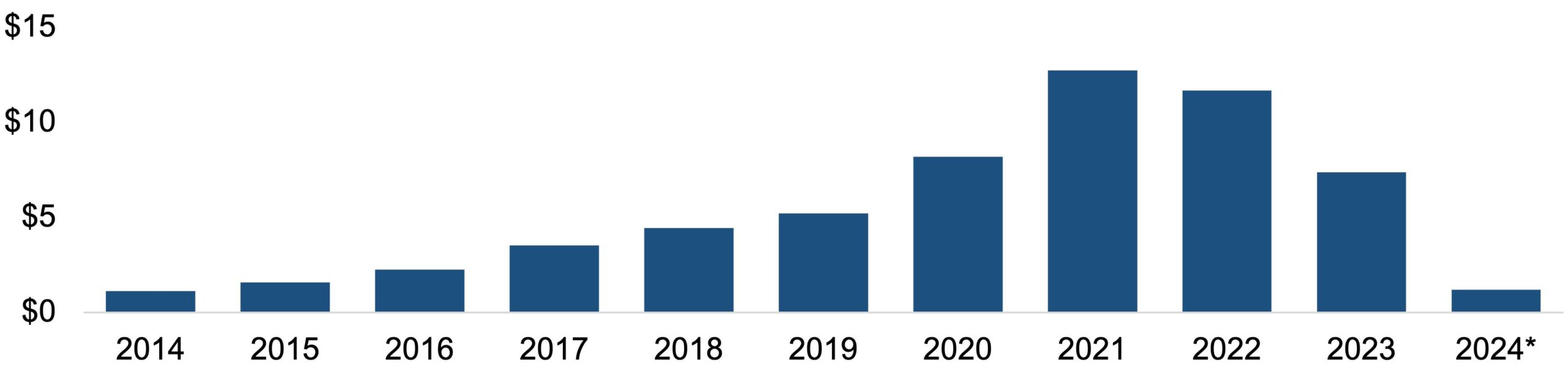

Agtech market is ripe for strategic consolidation and expansion

Exhibit 5: Global Agtech VC deal active (deal value in $b)

Source: PitchBook (Q1 2024)

With the venture capital boom of 2021 behind us, we see an opportune moment for growth equity funds (and hybrid private equity) to consolidate a market that received significant funding during 2020-2022. Many companies in the agtech sector are now facing challenges in securing additional VC money due to inflated valuations from that period, while investor focus has largely shifted towards AI technologies. By acquiring local champions or expanding into new product categories—such as diversifying into new crops or developing B2B channels—we believe this is a unique moment to combine forces and build a multi-continent, multi-channel, multi-product agtech leader.

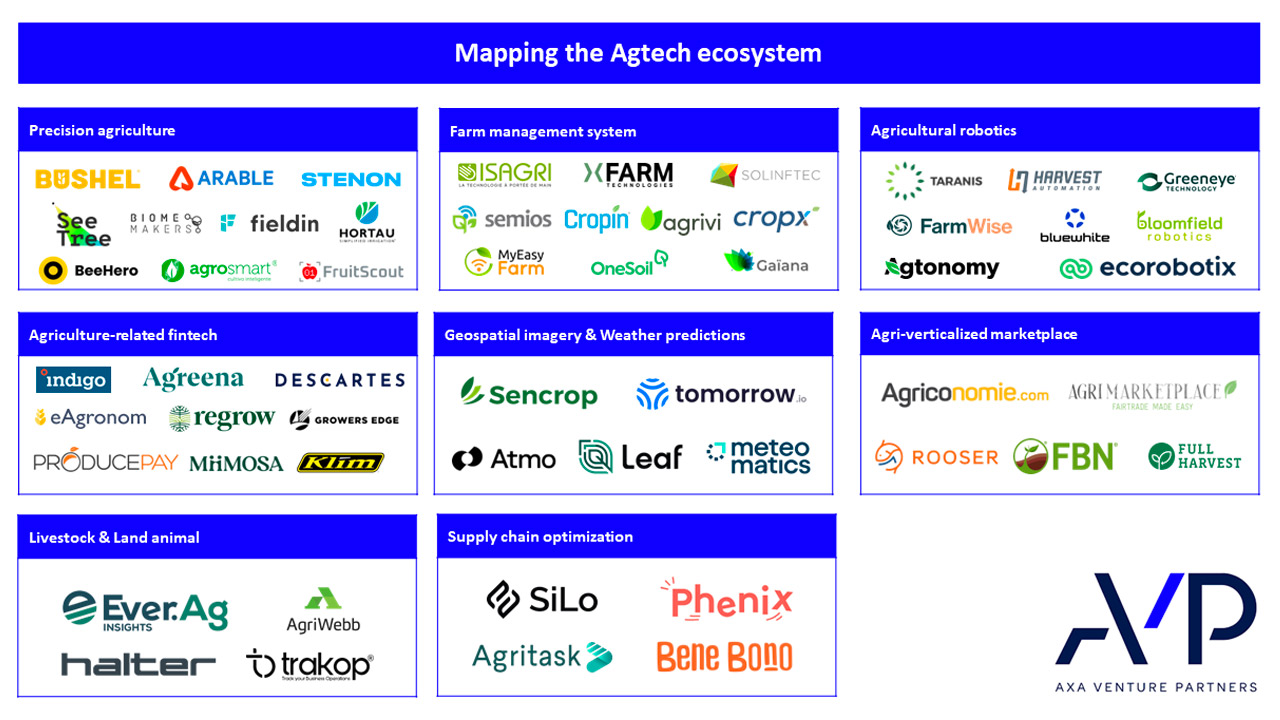

Mapping the Agtech ecosystem and presenting our Investment Thesis

Since we started our deep dive into the Agtech industry, we have connected with around 100 founders, investors, and industry stakeholders from all over the world and across different categories. Before we share our views on the Agtech landscape and its segmentation, I want to outline the thesis we have developed. Keep in mind, this comes from our perspective as a transatlantic growth investor with a focus on software-heavy investments.

- Unified data lake and orchestration tools: the integration of connected tractors, weather stations, moisture sensors, and satellite imagery has significantly improved farm efficiency but also added complexity to agricultural operations. We believe the agricultural industry needs a unified data lake or channel-agnostic orchestration tool that seamlessly connects these diverse data sources, simplifying data management and enhancing decision-making across farm operations.

- Simplification of communication and regulatory processes: agriculture is the most subsidized industries globally, resulting in significant administrative burdens for farmers who must navigate interactions with regional, national, and local bodies, as well as buyers. As the industry gradually shifts towards digital solutions, it is crucial to alleviate these burdens by centralizing communications and structuring data effectively. We believe this not only streamlines operations for farmers but also serves as a key engagement module within broader platforms, facilitating the integration of additional value-added solutions and ensuring that farmers provide the required inputs consistently.

- Value in Peer-to-Peer tools: similar to regulatory modules, we view peer-topeer communication platforms as essential tools for maintaining daily engagement with farmers. At the regional level, we have observed some players successfully implementing a freemium model, fostering communities around key issues such as weather data, pest control, staffing shortages, and equipment sharing. While we recognize that this approach can be costly in the short term, we believe a model akin to Waze’s success can be effectively adapted to agriculture, driving long-term value and engagement.

When it comes to go-to-market strategies, most players have developed their organizations and business models around a B2F approach. This is similar to a B2C or SMB product-led strategy, featuring a fragmented market, freemium models, and network effects. However, there’s a new wave of Agtech companies that are adopting or shifting to a B2B-first strategy. We actually prefer this model because it offers more stability and scalability. Plus, it avoids the need for door-to-door farmer acquisition, as B2B clients pay for these solutions instead.

We have summarized and segmented below the categories and most innovative companies we identified & met over this journey:

1. Precision agriculture

2. Farm management system

3. Agricultural robotics

4. Agriculture-related fintech

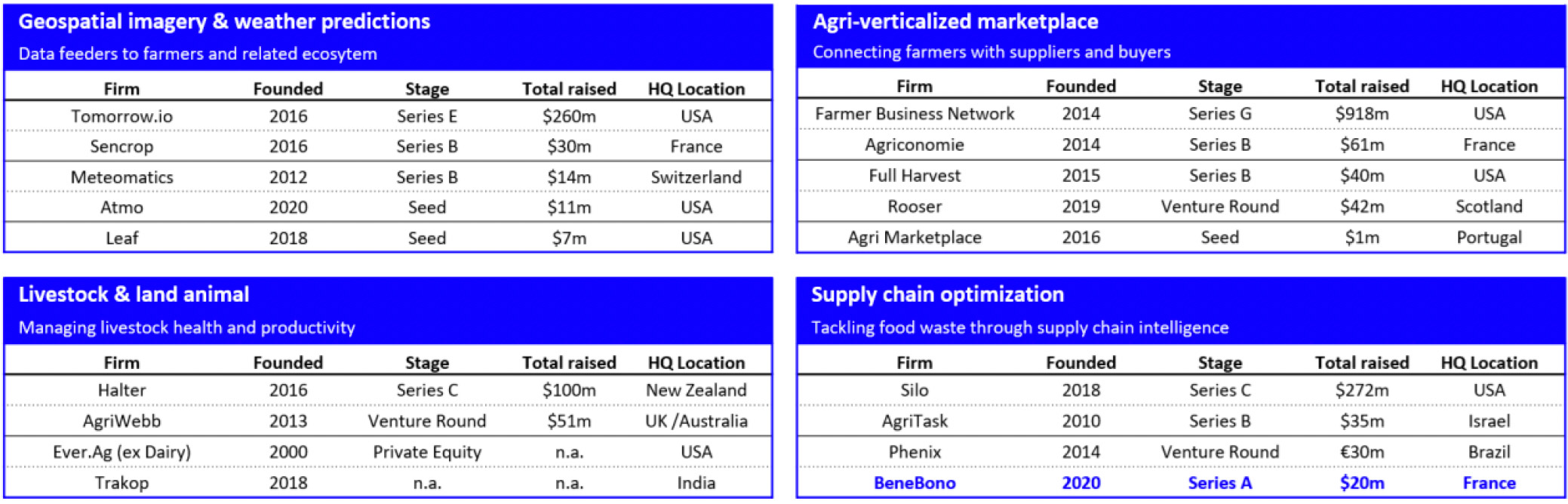

5. Geospatial imagery & weather predictions

6. Agri-verticalized marketplace

7. Livestock & land animal

8. Supply chain optimization

Few disclaimers:

– Our mapping is led by our investment thesis, with a focus on growth and softwareheavy companies. However, a few hardware-heavy players have been included in our list given the nature of the operations e.g. bucket 1 “drones & other robotics”,

– Companies have been categorized according to their core ag-related activity, although it should be acknowledged that no mapping is bound to be perfect as the categories are not completely hermetic. For example, Cropin and xFarm (included in bucket 3) also performs fintech-related agriculture services (bucket 4),

– We deliberately excluded vertical farming players and Ag biotech plays such as as Ynsect in France as it’s (I) extensively covered by fellow colleagues and (II) we felt it would obfuscate the mapping,

– Company stages and funding rounds have been sourced from the traditional VC databases (PitchBook and Crunchbase) as of June 2024, with unspecified rounds being decided upon by us