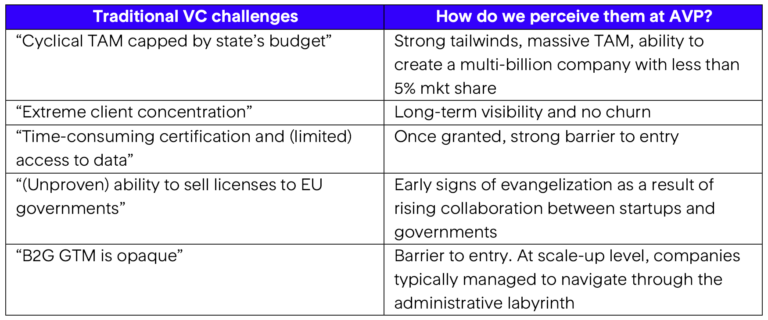

Geopolitical tensions, political interferences, reputational risks, perceived customer concentration and opacity of Business-to-Government (“B2G”) go-to-market: investing in the European defence tech industry is not for the faint-hearted.

Alexandre de Martino,

Associate, Atlantic Vantage Point

With war now back at the gates of Europe, it is becoming increasingly clear that Europe has let strategical competitors gain key asymmetrical advantages in technological warfare; the need for innovation is pressing! It is not surprising that last September, the Center for European Policy Analysis urged public policymakers to leverage the brain power of their startup ecosystem to spur emerging and disruptive technologies1; however, who will fund this gap? In our series, we wanted to approach this problematic via the lens of a traditional Venture Capital investor, understand generalist & not defence-focused.

While the area hasn’t yet been fully explored so far to the spotlight, we decided to study (first) and meet (second) with an onslaught of start-ups and stakeholders. Here are our key findings, notably highlighting what we called the “traditional VC challenges” and how do we perceive them at AVP:

Selling to governments: controversial? the apex of client concentration?

“There are some in our industry who view serving such agencies and missions as controversial. We do not. Regardless of our individual political beliefs, we all benefit from the work of the men and women in these agencies and the danger in which they put themselves daily. The least we can do is work to give back by building technologies that help them accomplish their missions more effectively and more safely.” Marc Andreessen at a16z summed it all in 2019 when he led his investment in Anduril, nothing to add, really.

In the US, defence and intelligence agencies are heavily fragments, the opposite tends to happen in Europe where they are more centralized: the State usually end up being the only payer in town. Extreme customer concentration is commonly perceived as a risk when valuing startups, but doing so in the case of B2G misses the true value of contracting with defence departments. It may be hard to get them onboard, but once they are in, they never churn. And while B2G contracting is not easily linkable to traditional SaaS metrics such as LTV, they grant unmatched long-term visibility to investors, and as more use cases are developed upsell is often guaranteed.

Lastly, while the growth of the TAM is capped by the State’s budget, it remains so gigantic that a multi-billion company can be built with less than 5% of market share.

Intellectual property and access to data

Traditional B2B SaaS investors and the military have different sets of expectations regarding software. Rather than paying on a recurring basis for licensed products, defence departments would rather acquire the entirety of the software all at once for obvious budget and security reasons. But as the CEPA’s points out, “intellectual property is the only profitable asset start-ups can claim”. We are confident that in the future government will find innovative ways to lease intellectual property. As a matter of fact, the recent Tornade contract awarded by the French MoD to Preligens marked the first time – to the best of our knowledge – that a European government accepted to pay for a licensed defence software.

While software and AI will be two of the great next value unlocks in defence2, they raise the ever-thorny question of data sharing with private contractors. Why should defence departments entrust 3-year-old companies with some of their most sensitive data? While this compels start-ups to train their algorithms with commercial data, effectively gaining the trust of the military constitutes a robust barrier to entry. Defence departments are far from being the most loquacious business partners, so being able to see around corners and predict their needs and use cases is auspicious.

Opacity of B2G go-to-market

In the current regulatory environment, each defence start-ups knows that it is dependent on a stage perhaps more critical than its technological proof of concept. It is the ability to win the trust of the military, and to navigate the labyrinth of administrative procedures to secure sought- after government contracts. This brings us to the paradox of defence innovation: while speed is determinant in technological competition, the military is historically more risk averse, which is incompatible with the rapid innovation cycles of venture capital. This put start-ups at a disadvantage against large contractors that have the knowledge, experience, and funds to navigate the lengthy and complex procedures (at least the outside-in perception) of government contracting. On the other hand, we recognize this as a strong barrier to entry in the event of success. At scale-up level, DefTech firms typically worked their way out of the maze, have a low risk of bankruptcy, and few competitors. On the latter, we expect this will be a winner take most market with 2-3 scaled players taking 65-70% of the market.

What about treating directly with large contractors? The indirect approach comes with its own set of risks, mainly a strong dependency on private actors and a weak bargaining position in case of acquisition. In this sense, we welcome the CEPA’s recommendation to develop more agile government contracting models. Beyond expanding opportunities for innovative companies, this would multiply the amount and frequency of defence VC funding by providing investors with more visibility on go-to-market.

Look out for our next piece, where we will be taking a deeper look at the landscape, highlighting some of the most innovative companies we met during the year.

Mapping the software Defence Technologies ecosystem

Since we began investigating the DefTech industry, we have had countless conversations with founders, investors, and professionals from the US, Europe and Israel. We soon discovered that finding a comprehensive infographic, particularly one with a software-heavy approach and European emphasis, was difficult.

So, here is ours; below are the categories and most innovative companies we identified/met:

1. Geospatial & Signals intelligence

2. Physical threat detection

3. Digital media analytics

4. Situational awareness & Combat management system

5. Communication & Virtual training

6. Decision intelligence & Predictive maintenance

7. Threat intelligence

Before this post is met with potential commentary about mis-categorization or omissions, a few disclaimers should be noted:

– Our mapping is led by our investment thesis, with a focus on software-heavy companies. Still, a few hybrid or hardware-heavy players have been included in our list e.g. Anduril (we felt it was intellectually wrong to exclude the most funded company in DefTech), or Lambda Automata (where hardware — an autonomous surveillance tower — will be the enabler to a future software solution)

– Companies have been categorized according to their core defence-related activity, although it should be acknowledged that no mapping is bound to be perfect as the categories are not completely hermetic. For example, Accrete (included in bucket 7) also performs social media intelligence (bucket 3)

– We deliberately excluded cybersecurity as (i) extensively covered by fellow colleagues and (ii) we felt it would obfuscate the mapping. However, there are few exceptions such as Shift5, which has been included for its data protection solutions of weapon systems

– Company stages and funding rounds have been sourced from the traditional VC databases (PitchBook and Crunchbase) as of December 2022, with unspecified rounds being decided upon by us

Be sure to check out our final piece, in which we will delve into the challenges associated with VC- backed DefTech exits, specifically focusing on the topical concerns surrounding sovereignty and ESG.

The challenges of exiting Defence Technologies

In our first piece, we discussed the “traditional VC challenges” associated with European DefTech investments. We chose to leave the exit topic aside, as we felt it requires a more comprehensive analysis. Not lying, the outlook may seem opaque at first; however, our work in this area, combined with early positive signs discussed below, leads us to believe that things are moving in the right direction.

Selling EU DefTech companies: navigating between sovereignty and value maximization

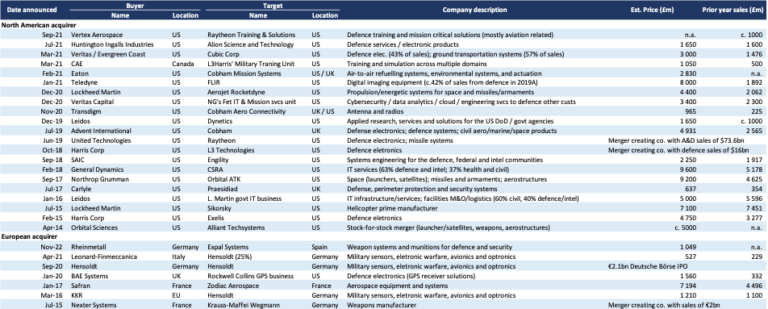

Exhibit 1: M&A transactions (above €1bn EV) in Europe and North America

Source: J.P. Morgan equity research (2022); MergerMarket; Company information; Press

Examining the past 10 years mega-deals (above €1bn EV) in Defence brings about some interesting conclusions, notably for future DefTech exits.

Starting with the challenges (from an European standpoint), it appears clear that deal activity is and will remain dominated by US strategic buyers for obvious reasons: bigger TAM, strategics with deep pockets, lack of cohesive defence strategy in EU, public markets being more receptive to mega-deals…the list is long. Additionally trans-Atlantic acquisitions are rare, unidirectional (US-to-UK, largely due to the history between the two countries), and highly scrutinized by regulators due to the fear sought-after technologies pass into foreign hands.

Therefore, as a VC investor, is banking on US strategic buyers the most suitable central exit scenario? Probably not.

Our French background reminds us of the recent Photonis case. The company, which specializes in photo-sensor imaging and night-vision technologies, is a true French military gem. In December 2020, the French State vetoed its purchase by the US Teledyne, likely due to protection of sovereign interests, and what we suspect was a lack of clear and ongoing communication among all stakeholders (including the French government). This resulted into a loss of value for the exiting investors, as HLD (French’s private equity) final offer ended up being a third lower than the €510m initially offered by Teledyne. Does this mean that we cannot count on EU strategic buyers for our exit scenario either? The answer to this question is likely to be more nuanced.

(Un)ability from EU strategics to write multi-billion checks to acquire, fast-growth but still break-even, DefTech companies will, in our view, remain a challenge as they end up trading on an EBITA, not revenues basis. However, when it comes to navigating the sovereign topics within the European Union, there is some cause for optimism: the German Rheinmetall acquired the Spanish Expal Systems in November 2022, and Leonardo (Italy) took a 25% participation in Hensoldt (Germany) in April 2021, considered as a very “hot” sell-side auction in Defence.

Are there any alternatives to relying solely on the five or so strategic buyers from the EU? In the absence of a liquid public market (today) for European DefTech companies, we believe Private Equity will play an instrumental role in the development of the industry. Ukraine’s invasion, abundant dry power and strong re-rating of defence stocks have stimulated the interest of investors and their lenders. We don’t see this renewed interest as an opportunistic one, as the definition of “defence assets” has broadened and there is an increasing number of dual-use applications.

IPO’ing EU DefTech companies: ESG, the “elephant in the room”?

No tables are needed to analyse the Defence IPO landscape in Europe.

According to our research, Hensoldt’s IPO in 2020 was the most recent since EADS (now Airbus) in 2000. I was lucky enough to participate in the construction of this success while I worked at JPMorgan – we supported KKR with its acquisition in 2016 until the 2020 listing. Today, Hensoldt has been a great success and there have been few similar successful IPOs since 2020. While external factors (macro tailwinds and scarcity of defence assets) and the intrinsic quality of the company played a massive role, the efforts of KKR should not be overlooked. As an investor, I want to remember that their hard work in fostering an ongoing and transparent dialogue with the German government was essential to this success!

On the positive side of the balance, US DefTech players such as Palantir or Planet (exposed to both civil and defence) will have a longer history of being listed and experiencing various market cycles. Anduril will also be listed when the IPO window opens again, providing an important reference for future DefTech IPOs.

Concluding this series of paper with the words of the Latvian deputy prime minister: “is national defence not ethical?”. In investor terms, are defence companies now ESG-compliant? “[While] this has long been a no-no for full-on ESG funds. It’s also been a bit of a no for most funds with a bit of an ESG overlay […] but it isn’t so simple” (Financial Times, March 2022). Today, the bias against defence stocks is not as clear cut as one would think.

For instance, Thales, Rheinmetall and BAE Systems have good ESG ratings while 6% of Hensoldt free float is currently held by ESG funds. Restrictions are mainly focused on specific products such as biological or chemical weapons rather than the sector as a whole.

Lastly, we are welcoming SEB IM’s decision to update their sustainability policy and allow for investment in defence again . Is this signalling a tectonic shift in the investor community? An investor survey from Deutsche Bank (2022) showed that 15% of North American investors still think defence should be excluded from ESG investments, while it jumps up to 57% in Europe! We believe European policymakers should take the lead in creating a more inclusive ESG environment.

1. CEPA, “Elevating our: a path to integrating emerging disruptive technologies”, September 2022

2. UK MoD “Defence artificial intelligence strategy”, June 2022

3. J.P. Morgan, « ESG Considerations », November 2022

4. SEB, « SEB Investment Management updates the sustainability policy for investments in the defence industry », March 2022