Mathilde Colli,

Associate

Introduction

Following the exuberant dealmaking environment of 2020-2021, venture capital (VC) entered a new phase. Rising interest rates and a less accommodating exit environment led to increased pricing pressure on valuations and a temporary slowdown in VC investment activity. At Atlantic Vantage Point, we have leveraged our proprietary data to analyse how VC investment activity trended post-2021 and the extent of funds’ valuation adjustments over the same period. Our study dives into the last eight quarters of capital call and portfolio data to provide you with privileged insights into venture capital activity over the last two years.

Deployment

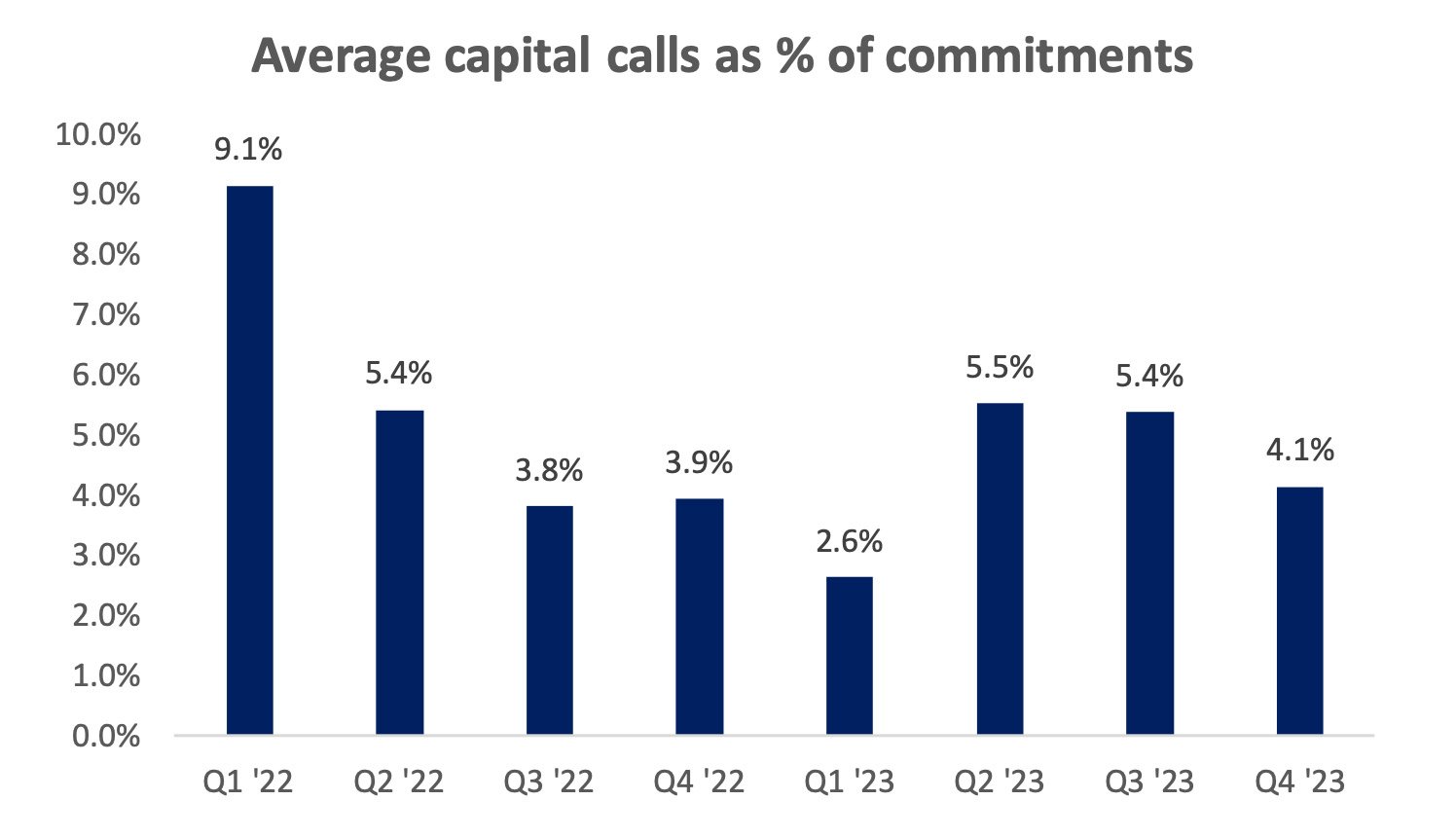

To analyse trends in deployment in 2022 and 2023, we used capital call data from the actively investing funds in our portfolio. Capital calls occur ahead of deployment and can be used as a leading indicator of investment activity in the broader market. As of Q4 ‘23, our sample included 31 active funds of which 24 were early-stage funds and 7 were growth-stage funds. We define early-stage as Seed to Series B and growth-stage as Series C+. By design, our portfolio is more concentrated on early-stage strategies, as they can be particularly attractive from a risk-reward perspective.

As a reminder, for a typical venture fund we would expect the investment manager to call ~5% of the total fund size per active quarter (i.e. during the investment period) on average. The actual expected capital call in each quarter also depends on the fund’s reserve ratio for follow-ons. We averaged quarterly capital calls as a percentage of total commitments across the funds in our sample to analyse trends in investment activity post-2021.

Capital calls as a percentage of commitment amounts peaked in Q1 ‘22, signalling the end of the 2021 hype period which was driven by heightened liquidity and an influx of nontraditional investors, such as hedge funds and mutual funds, into the VC asset class. Capital calls trended downwards to a low in Q1 ‘23 as the market slowed in response to less accommodating fundraising and exit environments. Since Q2 ‘23, there has been a recovery in capital call levels, signalling an increase in VC investment activity post-market correction.

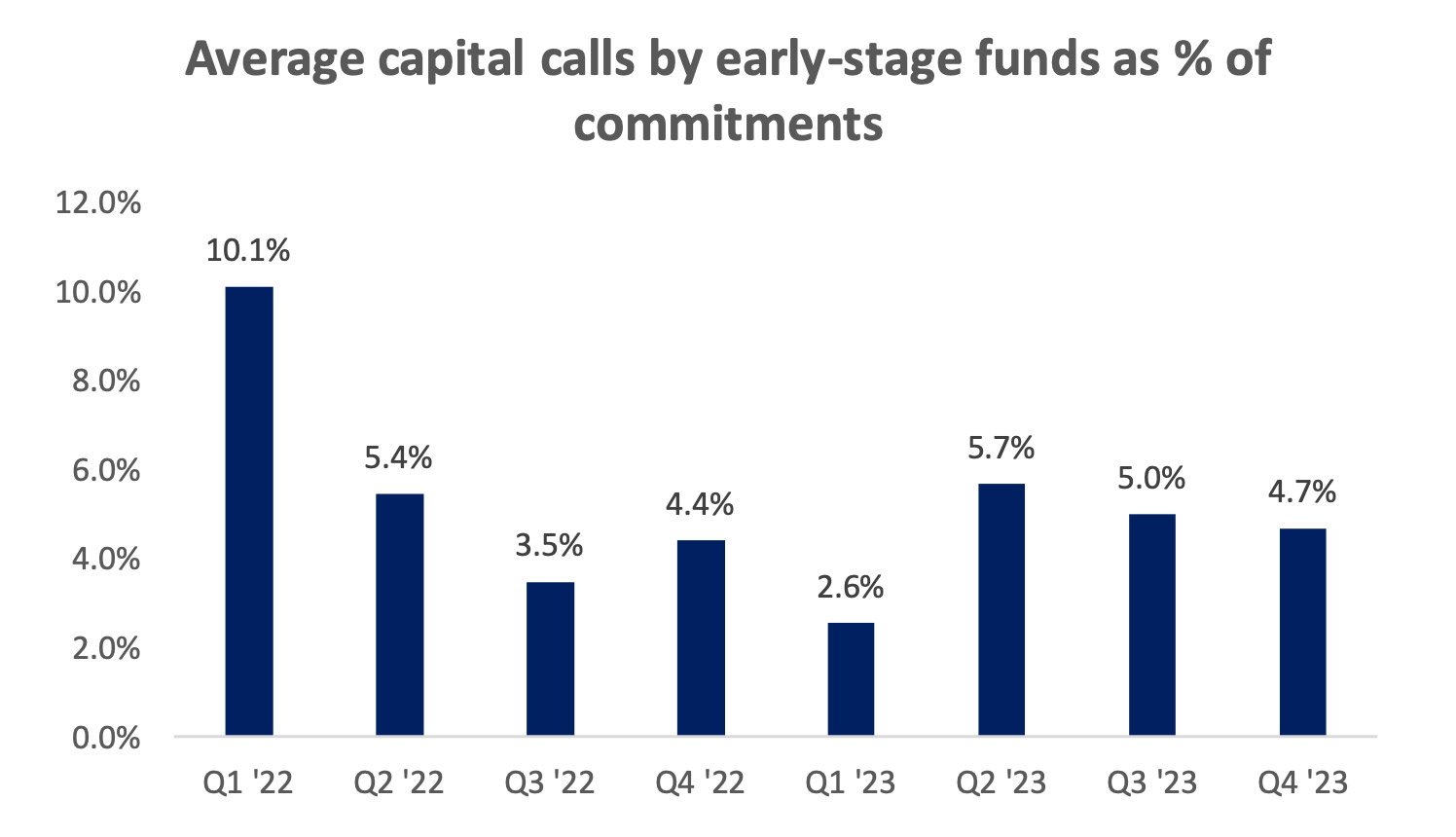

The recovery from Q2 ‘23 to Q4 ‘23 has been fairly consistent for the early-stage funds in our sample. The data points to a normalisation of investment activity in the early-stage VC market, with companies willing to raise at current valuation multiple levels and investors willing to deploy capital into these rounds.

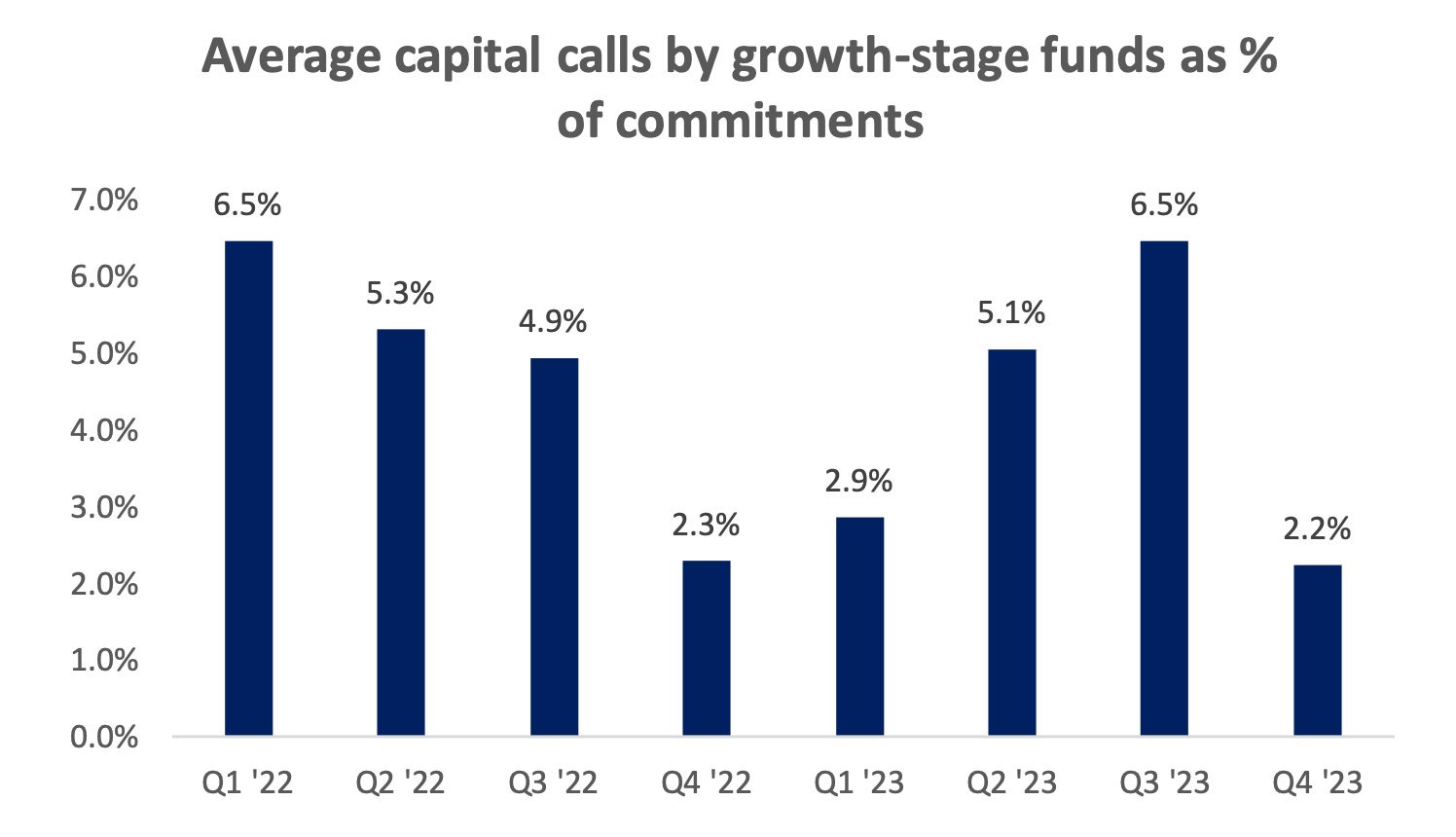

For our sample of growth funds, capital calls through 2023 were lumpier, and even fell below 2022 lows in Q4 ‘23. As of Q4 ‘23, the slowdown in later-stage investment activity is consistent with the pressure on later-stage valuation multiples and deal sizes, which led companies to prioritize extending their cash runways and achieving profitability over raising additional, potentially highly-dilutive funding.

We have not formally analyzed the extent to which capital calls were used for bridge rounds versus externally-led priced rounds. However, the overall decline in capital call levels across early-stage and growth-stage funds in mid to late 2022 was likely due to a reduction in the pace of new VC investments, given a more challenging macroeconomic environment. In 2023, early-stage funds’ capital call levels normalized. Continued volatility in capital call levels at the growth-stage is likely reflective of growth-stage managers’ bias towards best-in-class companies that have successfully grown into their valuations, limiting the volume of completed transactions to a relatively small proportion of mature companies that were fundraising in 2023.

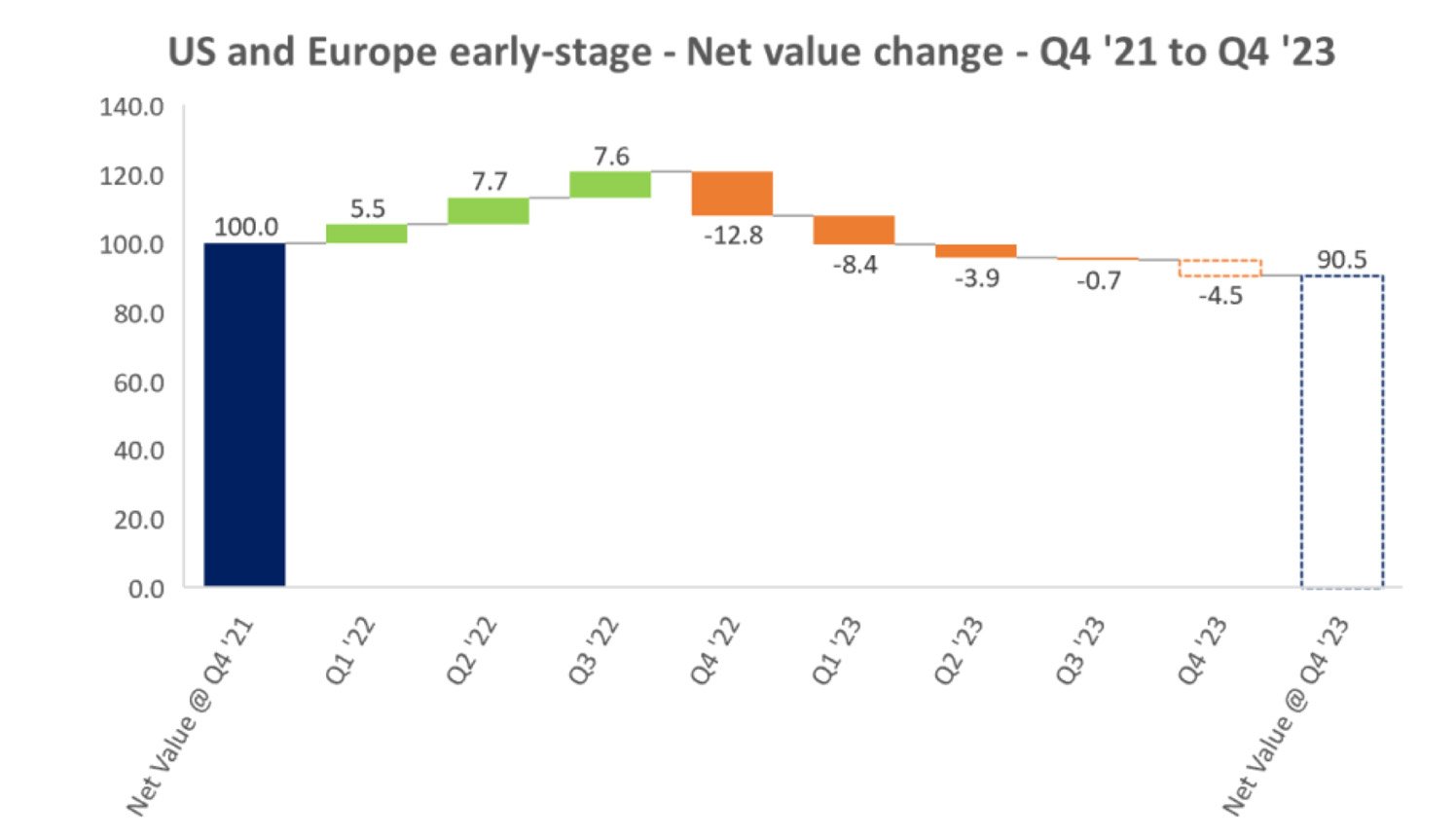

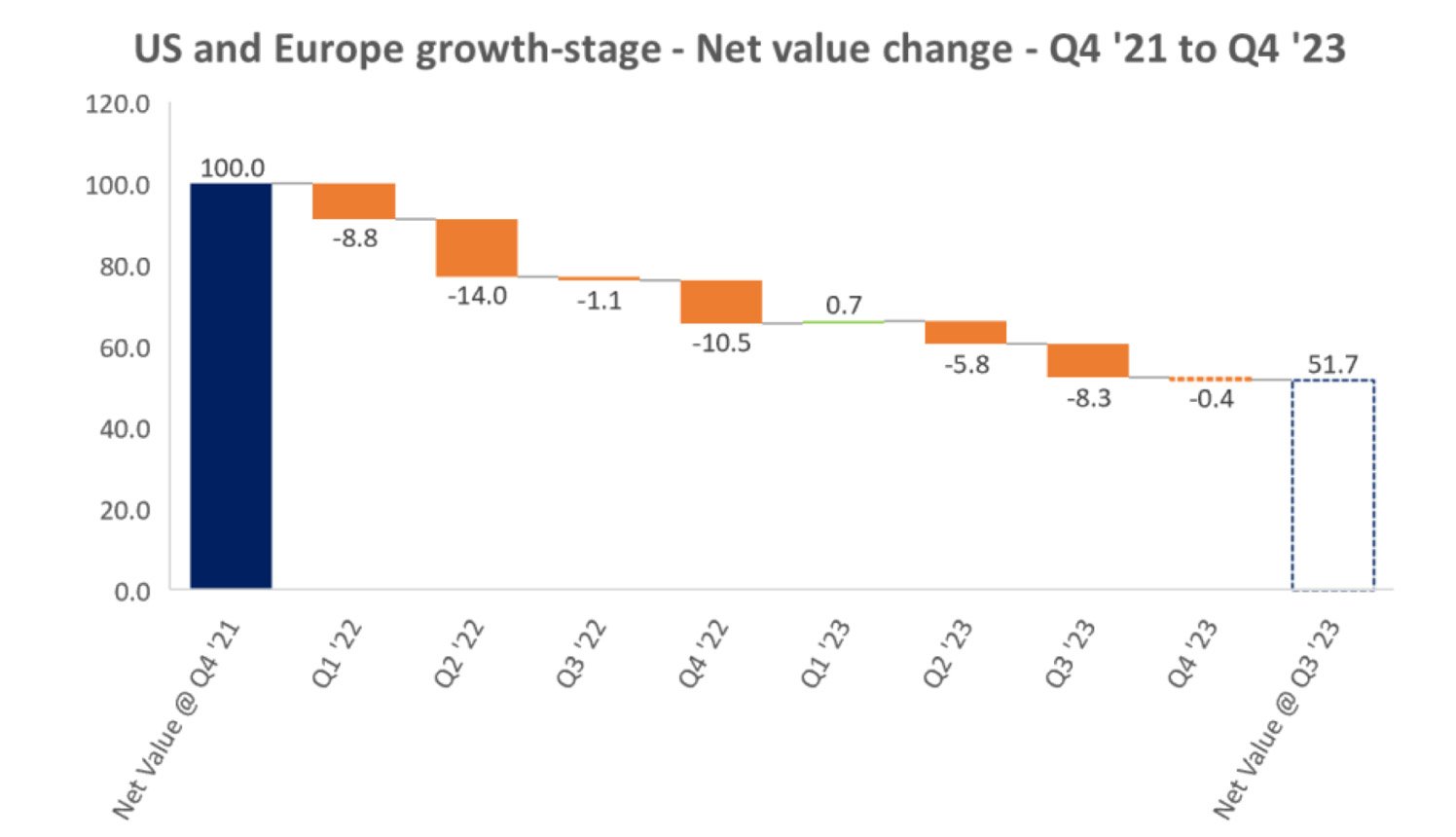

Net value changes

Changes in net value[1] provide additional information on the evolution of the VC market over this period. In order to understand how pricing pressures have impacted VC portfolios since 2022, we analysed quarterly net value changes for a sample of funds. Our sample includes US and Europe fund vintages from 2017 to 2020. The sample is split into early and growth. The early-stage group of funds includes 16 funds and the growth-stage group includes 6 funds. We constructed two equal-weighted net value bridges as an average of the underlying funds’ net values rebased to 100 at Q4 ‘21. Q4 ‘23 values are an estimate based on a subgroup of our funds that had already reported Q4 numbers as of this publication date.

Our early-stage sample shows that early-stage funds as a group were relatively stable over the two years to Q4 ‘23, with an average net write-down of -10%. The data indicates that for three out of eight quarters in this period, net write-ups outweighed net write-downs and overall early-stage valuations have been resilient post the period of exuberance in 2021.

The data on later-stage funds tells a different story. Net write-downs outweighed net write-ups in seven out of the eight quarters in this period, leading our sample to end 2023 with a net value -48% lower on average relative to the starting point at the end of Q4 ‘21. Net value write-downs reflect both discretionary haircuts applied by investment managers on their valuation marks and in other cases write-downs due to a company raising a “down-round” below the previous round’s valuation.

The stronger average performance of the early-stage funds in our sample makes sense given the relatively low volatility in early-stage valuations during the previous period. According to Pitchbook data, median pre-money valuations at pre-seed and seed in 2023 were near or above record annual highs, partly because the valuation step-up in 2021 was less drastic[2]. From 2019 to 2021, the median seed valuation increased by 28% compared to 74% at early stage, 68% at late stage, and 130% at growth[3]. The smaller step-up in seed and early-stage valuations compared to growth valuations during 2019-2021 helps to explain their resilience in 2022-2023. Valuation approaches for pre-revenue / early-stage businesses tend to focus on team, product, and long-term prospects, and consequently early-stage valuations are less impacted by market conditions and multiple expansion. In contrast, at late stage, the steep valuation step-up in 2021 was followed by larger write-downs in portfolios post-2021 as valuation metrics moved away from growth at any cost towards a greater emphasis on profitability.

Final remarks

The data presented here confirms that VC investment activity dropped in 2022, as many of our readers will know, but our analysis also reveals a divergence between the early and later stages of the market in the last two years. The data on net value reveals that on average early-stage portfolios have held up significantly better than late-stage portfolios in the two years after 2021. Early-stage investment activity also seemed to have normalized by Q4 ‘23 to a greater extent than late-stage investment activity.

It is important to note that our analysis is based on a limited sample size and is over-indexed on early-stage funds. Nonetheless, data from other sources such as Pitchbook corroborates our finding that the early-stage side of the market has been more resilient overall in 2022 and 2023. At the growth stage, we expect investment activity to remain below the heightened levels of 2020 and 2021. Activity levels should however revert to long-term averages due to the level of dry powder in the market with managers likely to have a bias towards concentrating capital to best-in-class companies globally, but this time at materially different valuations.

[1] Net Value change = (TV(n) – TV(n-1)) – (TC(n) – TC(n-1)) where TV(n) = Total Value in period n, TV(n-1)= Total Value in period n-1, TC(n) = Total Cost in period n, TC(n-1) = Total Cost in period n-1

[2] Pitchbook 2023 US VC Valuations Report, p.5

[3] Pitchbook 2023 US VC Valuations Report, p.6