In early February, I had the opportunity to connect with founders, operators and investors at the Manifest Conference in Las Vegas, which focused on highlighting recent innovations and advancements within the supply chain and logistics industry. Walking the conference floor, I met with exhibitors showcasing autonomous warehouse robots, electric vehicles and shipment tracking devices, among many others. While each company displayed a unique solution to a variety of different problems currently impacting the supply chain and logistics industry, a few key themes emerged after speaking with over 50 companies and investors at Manifest.

Ethan Volk,

Associate, Atlantic Vantage Point

Theme 1: Last-Mile Optimization Provides Both a Cost Saving and Point of Differentiation

The last-mile, or the transport of a package from a fulfillment center to its final destination, is often one of if not the most expensive pieces of the logistics puzzle (one survey noted that last-mile delivery can contribute upwards of 50% of the total cost of shipping)1 . Over the past two to three years, the combination of inflation, pent-up consumer demand, volatile fuel prices and labor shortages have only served to increase the cost of last-mile delivery (Figure 1 below provides an overview of the components of last-mile delivery costs).

Conversely, the last-mile can also prove to be the most valuable piece of the customer experience – the prime example of this is Amazon, which has been able to win over consumers by offering near- instant delivery with reliable delivery times and without compromising the quality of service. For three in four consumers, an excellent last-mile experience can lead to increased spending and brand loyalty2.

For organizations large and small, operational efficiencies in the last-mile can provide both a cost saving and a point of differentiation. Through both multimodal logistics networks and AI-powered software solutions, businesses can better serve their customers while also expanding their bottom-line profitability. Additionally, companies that maintain their own workforce of drivers or vehicles can benefit from intelligent route scheduling, dynamic fleet optimization and automated dispatching to increase driver and vehicle efficiency, ensuring that both drivers are more productive during their workable hours and vehicles are used to their fullest extent.

As businesses seek to find ways to boost margin and improve the customer experience in 2023 and beyond, optimizing the last-mile will be a key operational goal.

Theme 2: Real-Time Shipment and Supply Chain Visibility Are Must-Have Capabilities

For both businesses and consumers, it is no longer good enough to only know whether a package has left a fulfillment center or is simply out for delivery. For example, it is critical for a grocer to understand what happened to a shipment of strawberries on the way to its retail store – were they exposed to excessive light? What was the temperature and humidity during transit? Were they mishandled or damaged? For businesses exclusively dependent on last-mile delivery networks (e.g., Grubhub or DoorDash), providing real-time tracking of where delivery drivers are can help to improve customer service and reduce theft.

Tive is one of AVP’s portfolio companies that is providing a differentiated solution for real-time shipment tracking and visibility. Through a combination of proprietary hardware, software and services, Tive’s end-to-end solution captures and transmits shipment data in real time, alerting teams when something is amiss and providing reporting and analytics to better improve business processes.

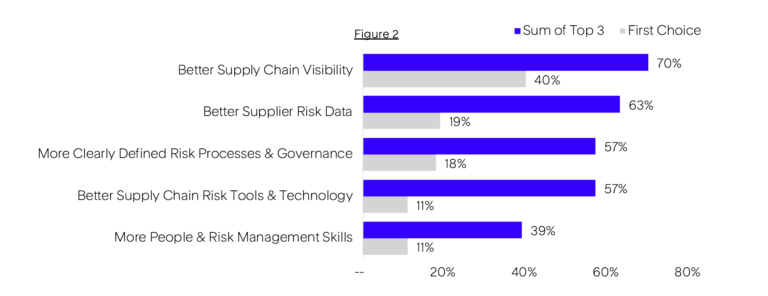

In addition to shipment visibility, organizations have continued to put a greater emphasis on visibility for their entire supply chain (Figure 2 below highlights the most important areas of improvement within supply chain risk management according to industry professionals)4. Supply chain visibility, or the objective of having a comprehensive view of an organization’s full supplier ecosystem including interdependencies and key risk areas, varies across the spectrum of suppliers. While supply chain visibility is much more common in Tier 1 suppliers which produce finished goods (80% have >70% visibility), Tier 3 suppliers of parts and raw materials have very little visibility into their entire supply chain (78% have <25% visibility)4.

Ultimately, the core issue is a data problem – a company’s end-to-end supply chain is often comprised of countless vendors stitched together through complementary processes and solutions, each with private operational data. Without a centralized data repository housing the relevant data from each supplier, it is nearly impossible to understand the dependencies of an entire supply chain network. To solve this, we believe that companies which can aggregate i.) public and private supplier data, ii.) enrich and analyze the data via AI / ML algorithms and iii.) produce both company-specific multitier supplier mapping and predictive analytics for organizations will succeed.

It is vital that the next generation of shipment and supply chain visibility companies not only provide data to their customers in real time but also offer proactive and reactive insights, allowing them to highlight and address issues early and often before they become consequential.

Theme 3: Unified APIs Will Augment the Supply Chain’s Existing Data Infrastructure

As noted above, an organization’s end-to-end supply chain is comprised of multiple constituents. Moreover, with each constituent of the value chain (e.g., shippers, carriers, distributors, suppliers) working with a different set of technological standards and business policies, data exchange and data interoperability pose significant challenges.

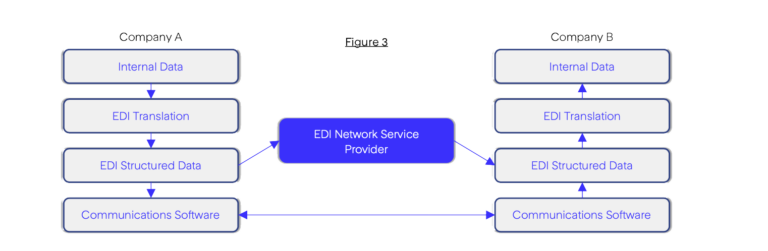

EDI – or electronic data interchange – has historically provided a solution to this problem. EDI digitizes and standardizes large quantities of physical documents and processes5, enabling businesses to exchange data electronically and maximize efficiency (Figure 3). However, with the continued acceleration of cloud technology, companies should consider migrating from legacy, on-prem EDI solutions in favor of modern cloud-native options.

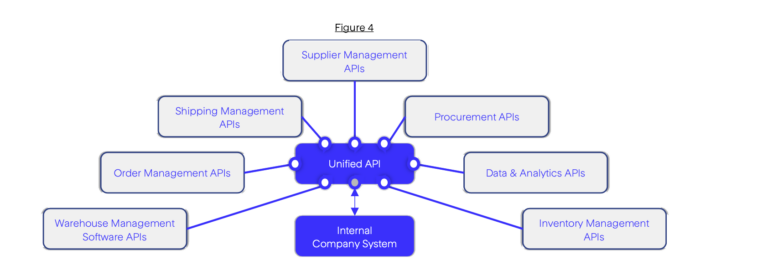

In addition, while EDI has long served as the standard within the supply chain, unified APIs (application programming interfaces) have seen increased adoption across several industries from human resources to financial services in recent years. Instead of developing custom-built API integrations on a case-by-case basis to connect into various software solutions, a unified API (Figure 4) can service as single endpoint, standardizing resources and data models through one centralized integration6.

While unified APIs might be seen as a replacement for EDI, there are benefits to using both technologies in tandem. A dual-track approach can ensure that companies match a partner’s technological capabilities, whether by connecting into their EDI protocols or API infrastructure. EDI and APIs also facilitate different use cases – EDI is better for highly secure, periodic updates such as processing confidential financial documents whereas APIs excel in enabling the real-time exchange of data to unearth actionable insights7.

As the suite of software solutions used by supply chain and logistics companies grows, unified APIs will be a critical piece of the data infrastructure tech stack.

Theme 4: Worker Shortages Will Drive Digital Transformation within Warehousing, Fulfillment and Worker Management

In 2022, nearly 60% of light industrial businesses saw an increase in fulfillment volume relative to 2021; at the same time, 73% of businesses (up from 26% in 2021) struggled to garner enough workers to capitalize on the increase in volume8. If the worker shortage continues to persist, businesses will be faced with two potential options – a) digitally transform their warehousing and fulfillment operations via software and automation and b) deploy solutions that improves worker retention, upskilling and reliability / safety.

From a software and automation perspective, employing a comprehensive, cloud-native warehouse and inventory management system can reduce complexity and allow workers to easily track, store and transport inventory within fulfillment centers. Additionally, end-to-end software platforms that facilitate more complex fulfillment use cases (such as cross-border trade and dynamic pricing) can help put parts of the logistics process on autopilot. Moreover, increasing fulfillment automation through both unified APIs and platform integrations can lead to added fulfillment efficiency. Within AVP’s portfolio, Sendcloud and Arta are focused on providing automation-driven, cost-efficient fulfillment experiences for e-commerce brands and sellers of high-value goods and collectibles, respectively.

From a workforce perspective, solutions focused on employee retention will prove to be of utmost importance given the current labor shortage. Moreover, companies providing software and services to support upskilling and career mobility for workers will further help to reduce turnover while also building an internal talent pipeline. Worker safety is also critical – as they say, the best ability is availability; AI and computer vision software deployed through warehouse cameras can assist in both catching accidents in real-time while also flagging problematic behaviors which could lead to future worker injury.

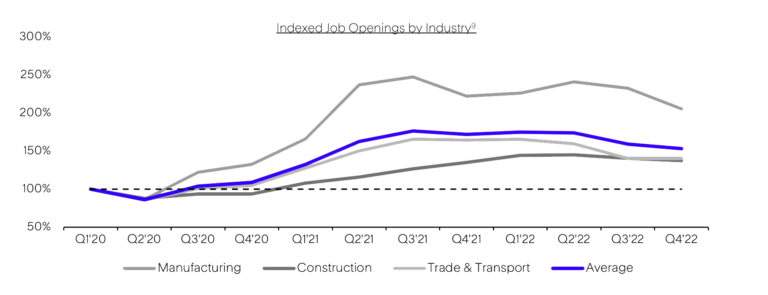

With job openings within manufacturing, construction, trade and transport still above their pre-COVID baseline levels, businesses will need to focus on solutions that allow them to do more with less, whether through digital transformation or improved worker efficiency.

Parting Thoughts

While these are only a few promising trends within supply chain and logistics, it’s clear that the sector has been on investors’ minds since the onset of the pandemic – investors deployed $24 billion in venture funding to startups in the space through the first three quarters of 2021 (+58% vs. the entirety of 202010). While funding and company valuations within both supply chain technology and the broader market came back down to earth in 2022, the passion and exuberance I witnessed from over 3,000 attendees at Manifest confirmed that there is continued excitement to build, fund and partner with the next generation of supply chain and logistics leaders.

At AVP, we have been fortunate to partner with some of the leading companies driving innovation within supply chain and logistics. If you’re an early stage or growth stage company actively building within the space, we would welcome the opportunity to meet with you – you can find me at ethan.volk@axavp.com along with the rest of my colleagues at avpcap.com.

1. Insider Intelligence, “The Challenges of Last-mile Delivery Logistics and the Tech Solutions Cutting Costs in the Final Mile”, January 2023.

2. Dropoff, “A Breakdown of Last-Mile Delivery Costs and How to Reduce Them”, February 2023.

3. Tive, “What is & What are the Types of Real-Time Visibility for Retail Supply Chain Management?”, April 2022.

4. Gartner, “Gain Supply Chain Visibility with Multitier Mapping to Boost Resilience”, February 2023.

5. Redwood Logistics, “The Differences Between EDI and API”.

6. Apideck, “What is a Unified API?”.

7. IBM, “The Future of EDI: An IBM Point of View”, February 2021.

8. FreightWaves, “Survey: 73% of Warehouse Operators Can’t Find Enough Labor”, February 2022.

9. FRED U.S. Economic Data, St. Louis Fed.

10. The Wall Street Journal, “Investors are Piling into Supply-Chain Technology”, December 2021.