Iyan Unsworth,

Vice President Fund of Funds

Introduction

It’s time to talk about the class of 2020-2021 tech IPOs and SPACs1. These are the companies that made their foray into the public markets during the 18-month period of exuberance, and at Atlantic Vantage Point, we have conducted an in-depth analysis of their performance whilst under public market scrutiny. Our study delves into the movements of their share price, market capitalization, and revenue multiples2 over time, providing a comprehensive summary of the performance trajectory of this “new breed” of public technology companies.

We understand that there have been numerous publications on IPOs and SPACs in recent times, but our team has unearthed some fascinating observations that will undoubtedly augment your understanding of the performance of these recently listed technology companies. The insights we have gathered are full of interesting nuances and we encourage you to take the time to read our study as it will be worth your while.

Sink or swim?

As you probably know, it’s been a tough year and a half for public tech companies. Some big names like Affirm, Rivian, and Coinbase are all trading at a hefty 70-90% discount to their IPO price and aren’t showing any signs of a full recovery just yet. But it’s not just those big players that are struggling – our data shows that the entire 2020-21 IPO/SPAC class is experiencing similar discount ranges:

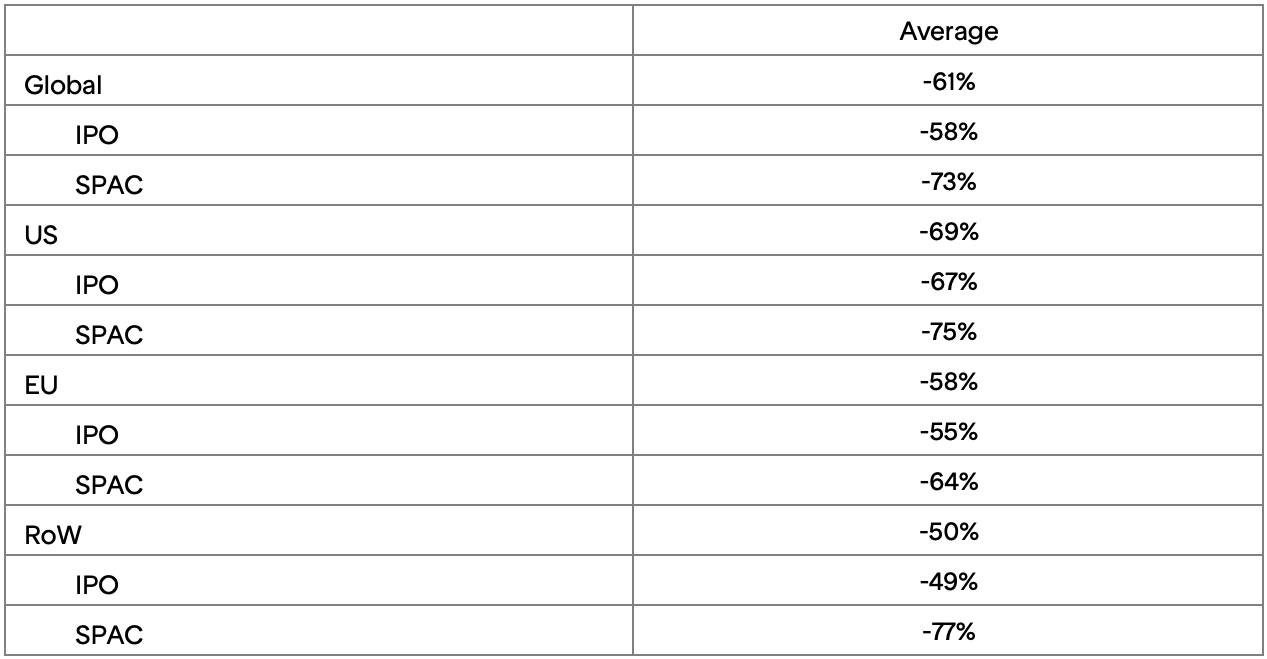

Share price % change since listing (as of 31-Mar-23)

If we take a closer look at our dataset, we can see that US companies have taken the biggest hit, with an average decline of 67% from their IPO price, while companies from the rest of the world3 (RoW) have fared a bit better overall, down only 49%. SPACs have performed worse than IPOs across all regions.

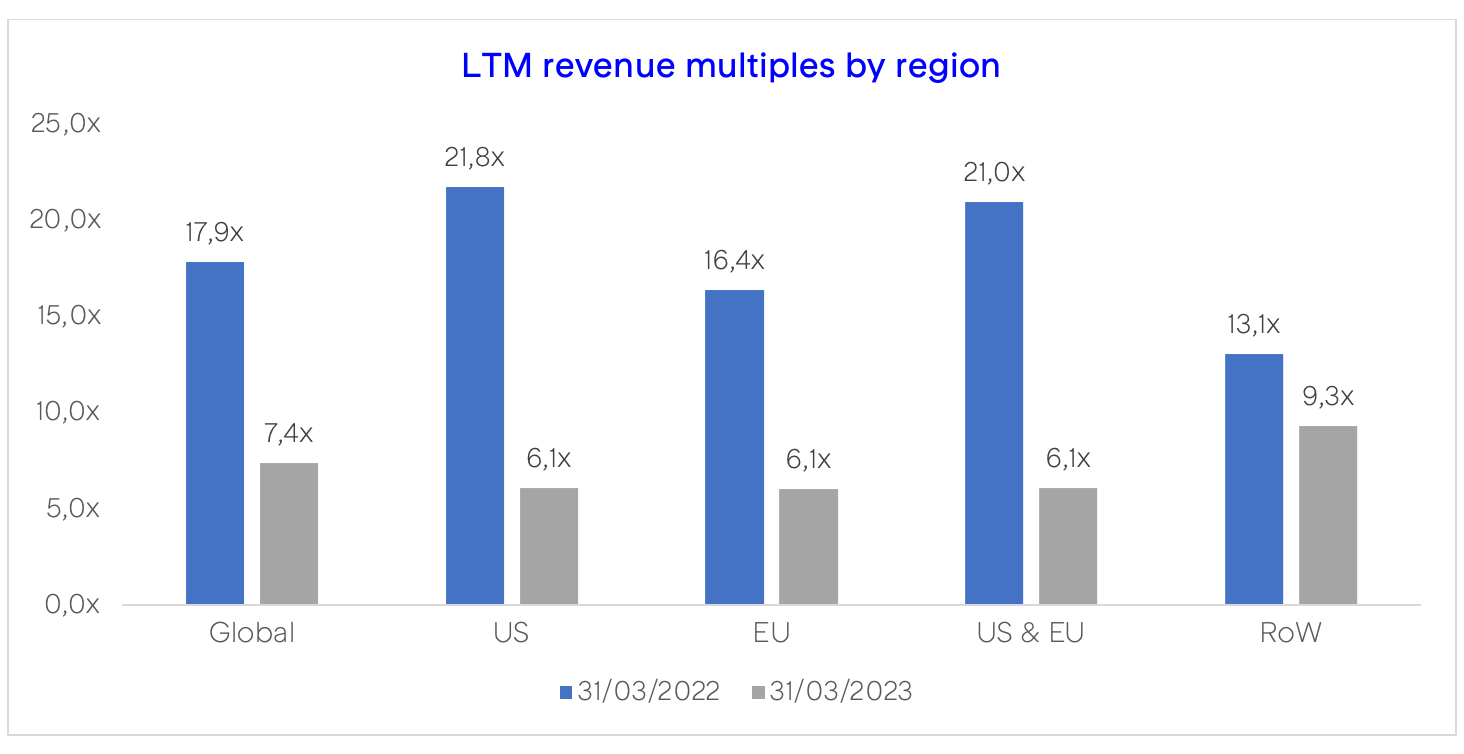

But that’s not all – when we look at the change in revenue multiples for these companies, we see a similar trend and reversion to the historical mean. Our global class of 2020-21 saw a decline from 17.9x in Mar-22 to 7.4x in Mar-23, which is a whopping 59% decline. And again, we see that US companies took the sharpest hit, with a decline from 21.8x to 6.1x, while RoW companies only declined from 13.1x to 9.3x.

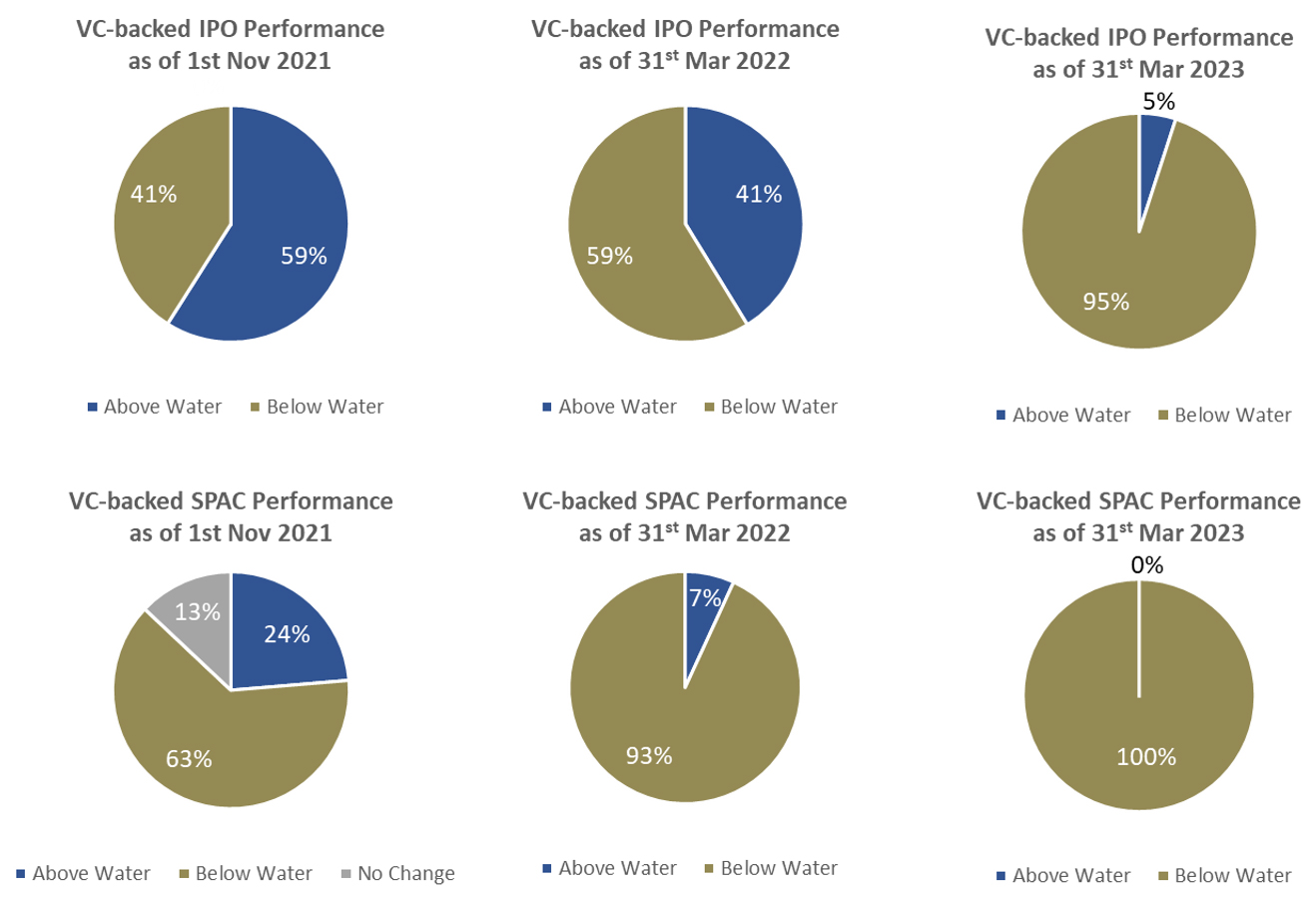

Looking at what proportion of the 2020-21 IPO/SPAC class are trading above or below their listing price at different points in time, we see that only 5% of companies were trading above their IPO price as of Mar-23. This is a jaw-dropping 54 percentage point decrease from market highs in 2021. The picture for SPACs is similarly bleak, with no SPACs trading above their listing price as of Mar-23. Overall, it’s been a tough time for the class of 2020-2021 tech IPOs and SPACs.

The underperformance of SPACs is likely to discourage more private companies and investors from going down this route to exit, at least until performance recovers to pre-crash levels – which, unfortunately, may be a long way off. We haven’t seen any real signs that the IPO window is reopening yet, although markets are starting to show some potential for a recovery in H2 2023 – H1 2024 (as we’ll discuss in the next section).

What has driven these share price fluctuations?

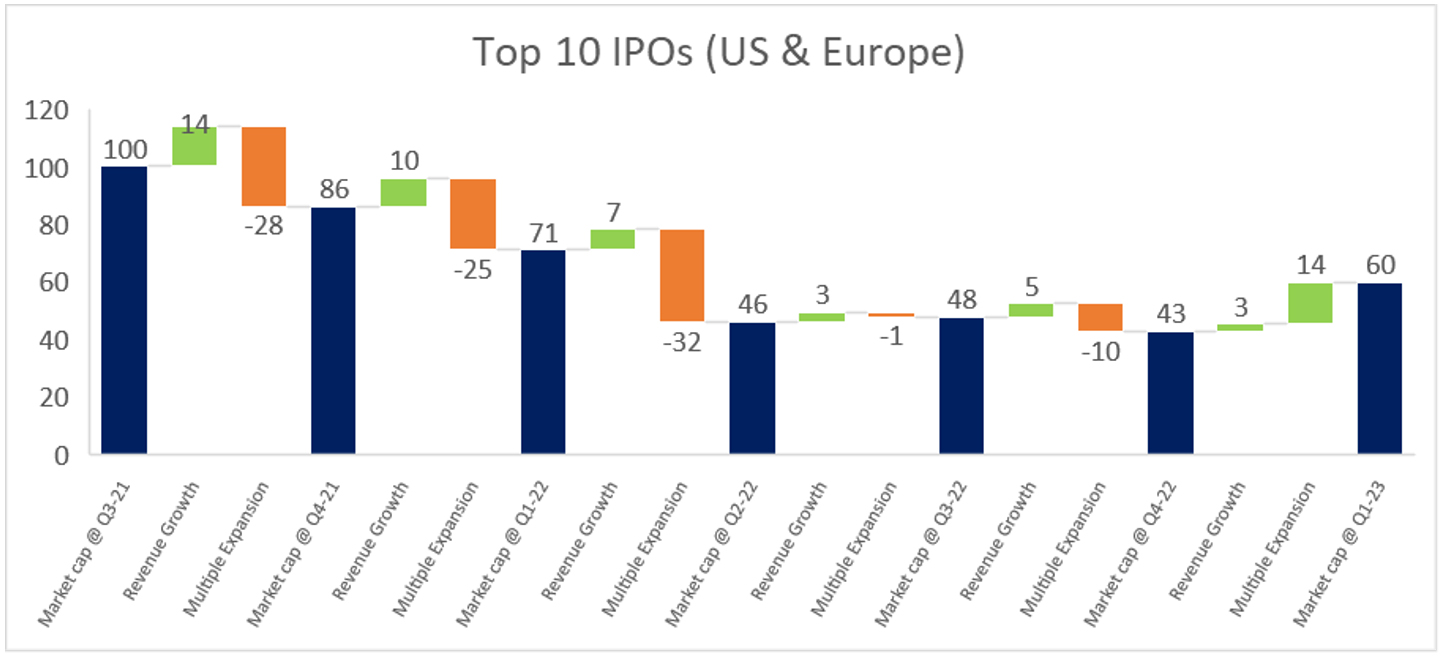

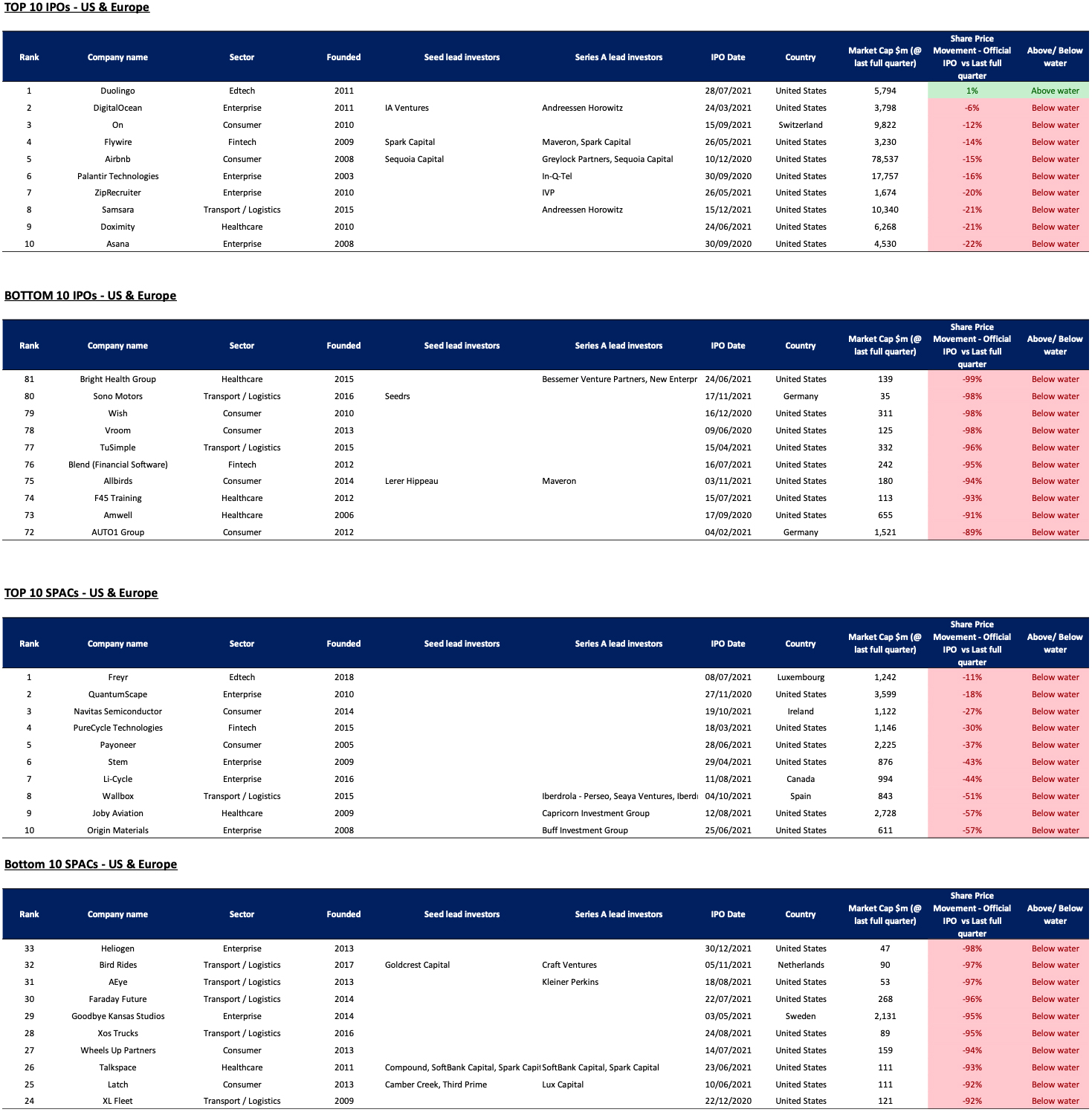

In addition to analysing the performance and valuation of the 2020-21 IPO/SPAC class, we also wanted to dive deeper and understand how investors are pricing these companies at any given quarter. To do this, we broke down the drivers of change in market capitalization over time, specifically looking at the top 10 US & Europe IPOs from the class (more detailed tables in the Appendix).

The resulting bridge chart4 offers a fascinating insight into the market’s behaviour. As we can see from the chart, the average market capitalization of these companies has gradually decreased from the rebase 100 in Q3-2021 to 43 in Q4-2022, despite continued revenue growth. This is due to a large, negative Multiple Expansion Value5 each quarter, which means that there was sustained multiple contraction, reflecting the shift from a momentum-driven pricing environment to a fundamentals-driven one.

Interestingly, Q1 2023 was the first quarter since the crash where we observed a positive Multiple Expansion Value for this subset of companies, which led to a notable increase in average market capitalization from 43 to 60. Could this be an inflection point for public tech companies? Are investors starting to price in risk again? It’s too early to tell from this smaller sample set of (arguably) high quality companies, but it is certainly a positive sign for the 2020-21 IPO/SPAC class.

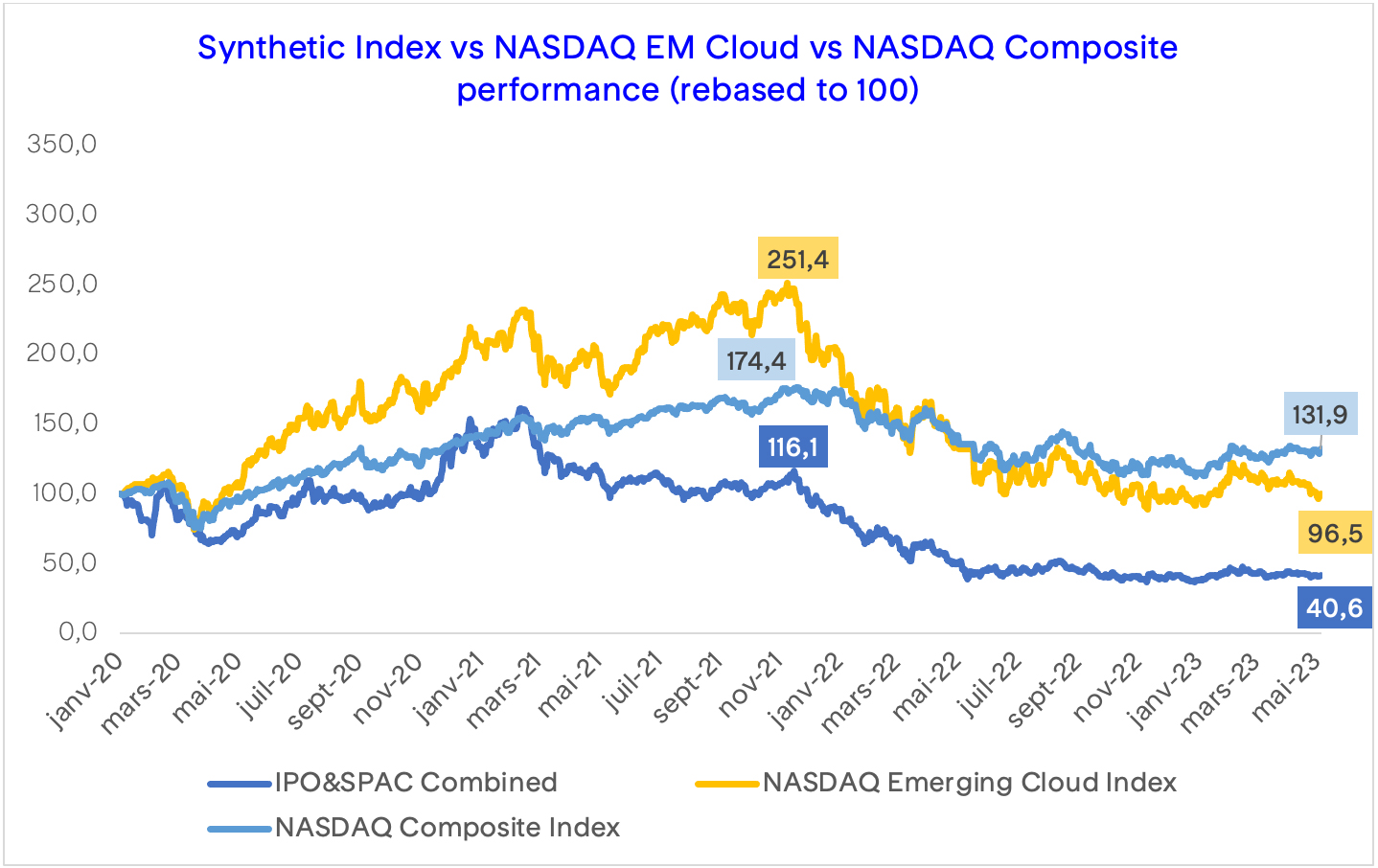

The Class of 2020-21 Synthetic Index

In order to gain a deeper understanding of the 2020-21 IPO/SPAC class and its comparative performance to other similar indices, the provided chart displays a synthetic index that is weighted by market capitalization of the entire class, alongside the NASDAQ Emerging Cloud and NASDAQ Composite. These three indices have been rebased to a starting point of 100 as of January 2020.

Upon analysing the chart, it is apparent that the synthetic index has been the weakest performer of the three, with the NASDAQ Emerging Cloud ranking second, followed by the NASDAQ Composite. This can be attributed to the lacklustre performance of technology companies in the public markets, particularly newly listed ones, over the last 12-18 months. If we further scrutinize the chart, it becomes clear that the NASDAQ Composite did not emerge as the top-performing index until May 2022. At its November 2021 peak, the NASDAQ EM Cloud was up 251% since January 2020, compared to the NASDAQ Composite’s 174%.

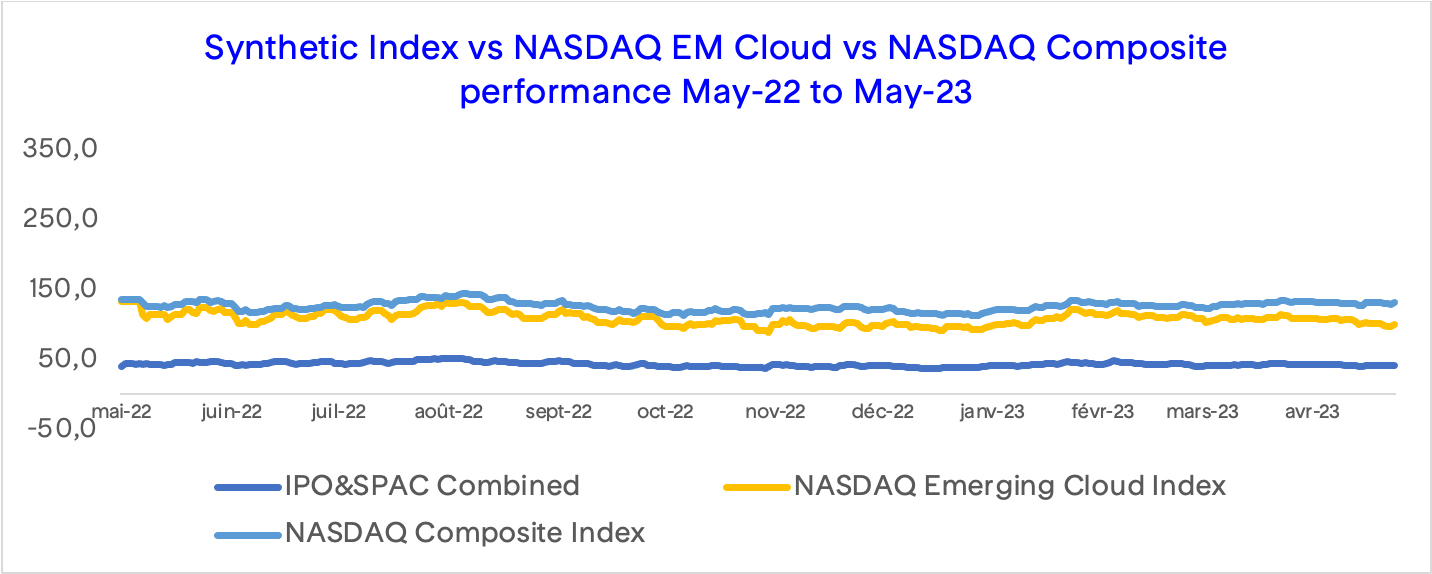

Interestingly, the synthetic index has consistently underperformed relative to the other two indices, almost always following a similar trend to the NASDAQ EM Cloud, which is not surprising given that the latter has a greater weighting towards more recent tech IPOs. Focusing on the last twelve months, we can observe that all three indices have remained relatively flat:

This may suggest that the market has bottomed out and a rebound is imminent. It will however be necessary to monitor the upcoming quarters to obtain more clarity before making any major inferences.

Final remarks

While some of the insights derived from this analysis may not be surprising to those closely following the tech industry, the availability of concrete data to confirm our suspicions undoubtedly carries value. The presented data is particularly compelling, revealing a significant decline in share prices among the 2020-21 IPO/SPAC class, with most companies trading well below their listing price. However, the Q1-2023 data brings a glimmer of hope, suggesting a positive multiple expansion following a prolonged period of multiple contraction. This potentially signifies a shift in the market’s risk appetite, moving away from the dominant fundamentals-driven approach of the past 18 months.

Recent impressive performance by renowned Big Tech players like Meta, Alphabet, Microsoft, and the newly inducted member of the $1tn club, Nvidia, support our view. These companies have exceeded expectations in Q1 2023, thanks to AI advancements that have reignited investor enthusiasm for growth. Moreover, there is additional optimism fuelled by indications that the Federal Reserve might be scaling back its pace of interest rate hikes in the near future. The recently secured US debt ceiling deal also deserves mention as it has helped avert another potential market catastrophe.

It is important to recognize that the positive signals in our analysis stem from a limited sample of higher-performing companies in our dataset. We have yet to witness widespread improvement across the entire cohort. Consequently, we anticipate that pricing for the 2020-21 IPO/SPAC class will remain relatively subdued until we observe tangible improvements in underlying demand, including lower churn rates, the expansion of existing customer accounts, and shorter sales cycles.

1. This study group consists of 183 VC-backed technology businesses (globally), split into 152 IPOs and 31 SPACs, that listed during the period of market exuberance (Jan-20 to Dec-21) with a market cap of over $1bn at the time of listing and for which reliable IPO issue share price data was available;

2.Defined as Market Cap/Last Twelve Months Revenues; 3. Includes China, Singapore, Israel, Taiwan, South Korea, Bangladesh, Australia, Japan, Thailand, Indonesia, Uruguay, Brazil, India, New Zealand, Kenya, Hong Kong, Russia, Saudia Arabia, Sri Lanka

3. Includes China, Singapore, Israel, Taiwan, South Korea, Bangladesh, Australia, Japan, Thailand, Indonesia, Uruguay, Brazil, India, New Zealand, Kenya, Hong Kong, Russia, Saudia Arabia, Sri Lanka

4. We have rebased the market caps for the top 10 IPOs to 100 as of Q3 2021. We are then showing their average Revenue Growth Value and Multiple Expansion Value in aggregate quarter-on-quarter to derive the adjusted market cap at the end of each quarter. ; 5. Revenue Growth Value = (Revenue in period 2 – Revenue in period 1)*Revenue multiple in period 1. Multiple Expansion Value = (Revenue multiple in period 2 – Revenue multiple in period 1)*Revenue in period 2;

Appendix

Data Leads

Liam Lewin O’Cuinn,

Associate

Mathilde Colli,

Senior Analyst